Pitch Deck Mastery

The capstone, where every prior analysis becomes one slide in a single argument to an investor. How investors actually read a deck (the read-alone and live tests, and the six questions every slide must serve); why the founding team carries the earliest decision and how to build the team slide; the standard slide sequence and the practitioner rules that shape it; the market-size slide and why a bottoms-up build earns trust; the team and traction slides; the financial slides as the analytical centerpiece (unit economics, driver-based projections, and burn and runway); the ask slide as a capital-structure negotiation sized by the milestone framework; and the seven ways founders destroy their own pitches, with four interactive calculators that carry the course's analysis onto the slide.

145 min

26

48

4

Learning Objectives

By the end of this chapter you should be able to:

- 1Explain why the pitch deck is the capstone where the market, unit-economics, valuation, cap-table, and capital-structure analyses converge into a single argument to an investor.

- 2Apply the two tests a strong deck should pass: the read-alone test when forwarded with no narrator, and the live-presentation test.

- 3Identify the six questions an investor is silently asking, and ensure every slide serves at least one of them.

- 4Explain the evidence that the founding team carries the earliest funding decision, and build a team slide that argues founder-market fit.

- 5Order the standard slide sequence by the weight of the investor question each slide answers, applying the Sequoia sequence and Kawasaki's 10/20/30 rule.

- 6Build a credible market-size slide from a bottoms-up TAM/SAM/SOM build rather than a top-down industry figure.

- 7Construct the traction and financial slides (unit economics, driver-based projections, and burn and runway) so every number is dated, bounded, and defensible.

- 8Size the ask with the milestone framework and price its dilution correctly on the post-money valuation, treating the ask slide as a capital-structure negotiation.

- 9Recognize the seven ways founders destroy their own pitches, and apply the FIN143 integration checklist and the two final tests before sending a deck.

Part One: How Investors Read a Deck: Two Tests and Six Questions. Section 1 of 8.

Part One · How Investors Read a Deck: Two Tests and Six Questions

How Investors Read a Deck: Two Tests and Six Questions

Part One

How Investors Read a Deck: Two Tests and Six Questions

The deck is where every prior analysis meets the investor. This part covers the two tests a strong deck should pass (the read-alone test and the live test) and the six questions investors silently screen for as they read.

The Pitch Deck Is Where Every Prior Analysis Meets the Investor

A pitch deck is not a new piece of analysis. It is the layer that compresses analysis you have already done into a form an investor can evaluate in minutes. By the time a founder builds a deck, the real work is finished: the market has been sized, the unit economics have been modeled, the cap table has been drawn, and the financing plan has been chosen. The deck takes the conclusions of that work and sequences them into a single argument. This is why the deck is the natural capstone of an entrepreneurial finance course. It does not replace the venture economics, the valuation, the cap table, or the capital structure decision. It carries each of those conclusions forward and puts them in front of the person who will fund them.

The consequence is direct. A deck cannot be stronger than the analysis behind it. A founder who has not built a defensible market model cannot present one. A founder who has not computed honest unit economics will either omit them or invent them, and investors are practiced at spotting both. The deck is a compression layer, not a disguise. When founders treat it as a disguise, adding polish to cover thin analysis, they produce the exact document experienced investors are trained to distrust.

Two Tests Every Deck Must Pass

A deck faces two separate evaluations, and it must survive both. The first is the read-alone test. Most decks are not presented; they are forwarded. A partner receives the file, opens it without the founder present, and forms a judgment in a few minutes. On that read there is no narrator to explain a confusing slide, no chance to clarify a number, no voice to supply the context a slide leaves out. Each slide needs to carry its own meaning at a glance.

The second is the live test. In a meeting, the same deck becomes a scaffold for a spoken pitch. Here the founder narrates, and the slides should be lean enough to support the story rather than compete with it. A deck overloaded with text fails the live test because the audience reads instead of listening. The design tension between the two tests is real: the read-alone version wants enough on each slide to stand alone, and the live version wants little enough that the founder carries the room. Strong founders resolve this with a clean core deck and a separate appendix, so the forwarded file is self-sufficient while the presented file stays spare.

What The Evidence Shows

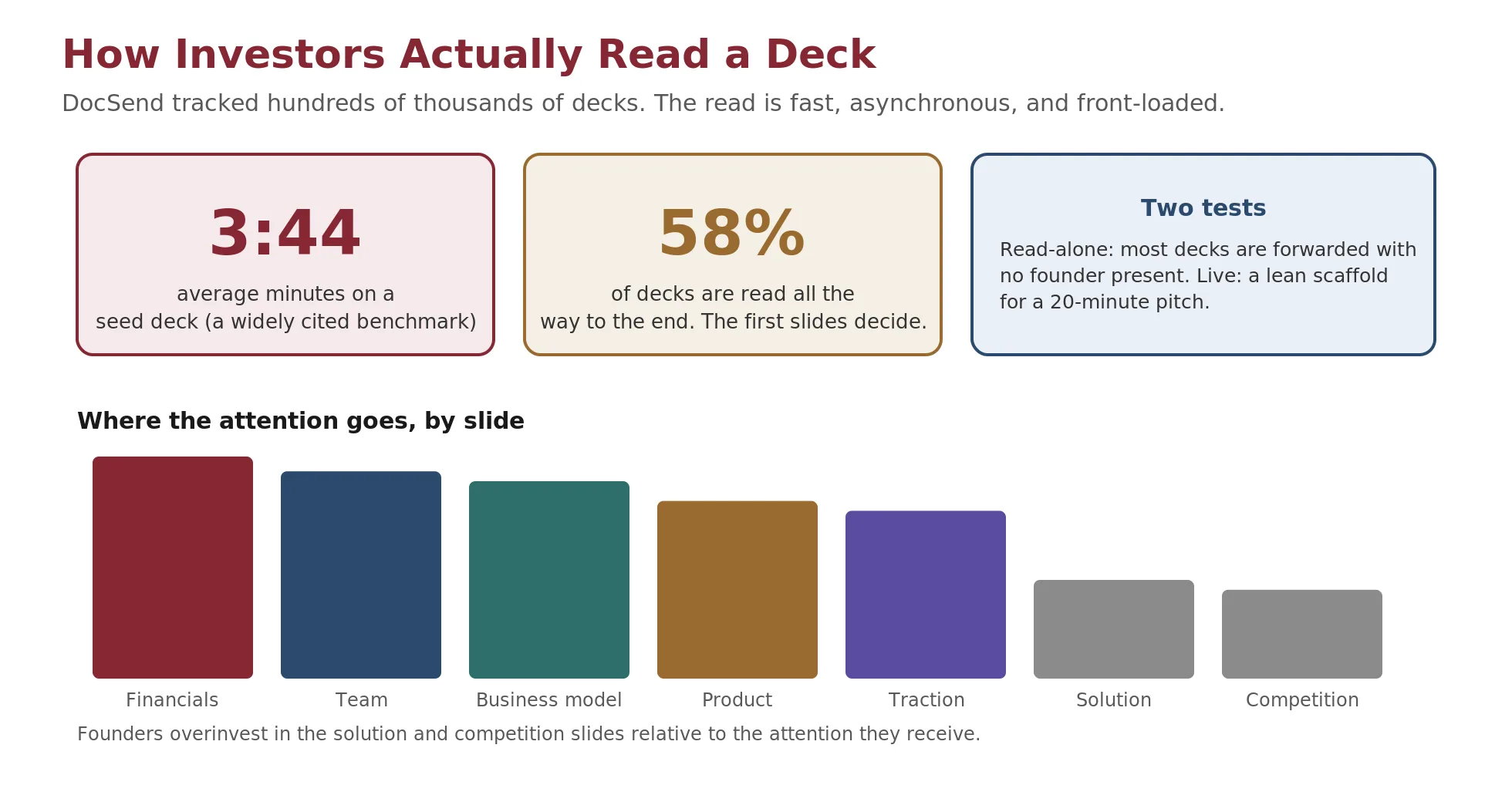

DocSend, which hosts and tracks investor deck views at scale, has repeatedly found that the read is fast and often incomplete. Investors spend on the order of a few minutes on a seed-stage deck, and a large share of decks are never read to the end. The practical implication is not that founders should write less, but that they should order ruthlessly. The slides that answer an investor's largest questions belong early, while attention is still high.

The figure records two findings that anchor the rest of this module. Investors spend an average of roughly three minutes and forty-four seconds on a seed deck, a figure DocSend has reported and that has been widely cited since. Only about 58% of decks are read all the way through. Attention concentrates on the financial, team, and business-model slides and thins on the solution and competition slides, which is the reverse of where many founders spend their effort.

Check Your Understanding

Knowledge Check 1

Pitch Decks & Fundraising Narrative

A founder has already built a market model, a unit-economics model, and a cap table. What is the distinct job of the pitch deck?

Knowledge Check 2

Pitch Decks & Fundraising Narrative

A deck is being forwarded internally at a fund with no founder attached. Which design principle matters most for that read?

Investors Screen for Six Questions, and Every Slide Must Serve One

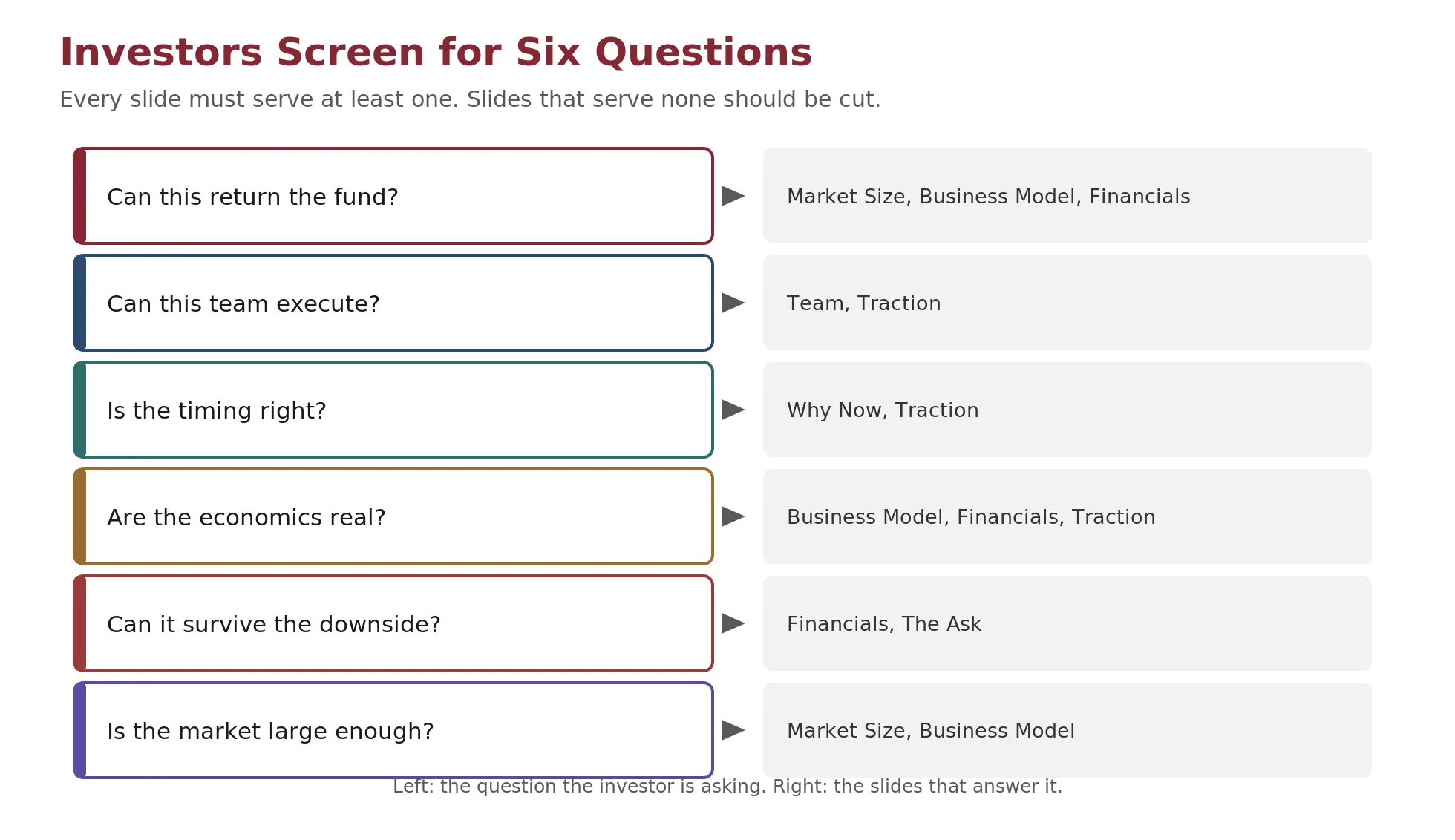

An investor reading a deck is not absorbing it neutrally. Behind the polite attention is a screen: a short list of questions the deck must answer before the investor will take a meeting, and a shorter list still before the investor will write a check. Six questions capture most of that screen. When a founder understands them, the deck stops being a tour of the company and becomes a set of answers. Each slide earns its place by advancing at least one of the six. A slide that advances none is not neutral; it is a cost, because it spends the investor's scarce attention without moving the decision.

The Six Questions

- Can this return the fund? A venture investor does not need every company to succeed; the fund's economics depend on a small number of investments becoming very large. The investor is asking whether this company could plausibly be one of them. This question ties directly to the power law studied in the venture economics module: because returns concentrate in a few winners, each investment is judged on whether it alone could return the whole fund.

- Can this team execute? Capital is abundant and ideas are cheap; the constraint is a team that can turn a plan into a company. The investor is testing whether these specific founders can build what the deck describes.

- Is the timing right? Most good ideas were tried before and failed because the market was not ready. The investor wants to know what has changed, in technology, regulation, or behavior, that makes now the moment this can work.

- Are the economics real? A growing top line is not the same as a viable business. The investor is checking whether each customer generates more value than it costs to acquire and serve, and whether that improves with scale.

- Can it survive the downside? Not every plan works as drawn. The investor is asking whether the company has enough runway and enough optionality to survive a slower ramp, a missed milestone, or a harder fundraising market.

- Is the market large enough? A company can execute flawlessly and still be a poor venture investment if the market caps out too low. The investor wants a market whose size can support a fund-returning outcome.

The mapping below shows which slides carry the weight of each question. It is also a cutting tool: build the deck, then ask of every slide which of the six it serves. The slides that serve none are the first candidates to move to the appendix or delete.

| Investor question | Slides that answer it |

|---|---|

| Can this return the fund? | Market Size, Business Model, Financials |

| Can this team execute? | Team, Traction |

| Is the timing right? | Why Now, Traction |

| Are the economics real? | Business Model, Financials, Traction |

| Can it survive the downside? | Financials, The Ask |

| Is the market large enough? | Market Size, Business Model |