Capital Structure

The financing decision: whether a company should raise debt, equity, or a hybrid, and at what cost. Why capital structure is a founder's highest-stakes financial choice; how Modigliani and Miller set the frictionless baseline and then break it with taxes; the tradeoff theory that balances the interest tax shield against distress; the pecking order under asymmetric information; the agency-cost and signaling forces that shape the choice; the weighted average cost of capital and why a startup's cost of equity is dilution; the debt instruments available to startups and the tax-shield caveat; how the capital stack evolves across the lifecycle; when venture debt extends runway and when it becomes a cliff; and the control, signaling, and rich-versus-king dimensions beyond money, with four interactive calculators.

120 min

25

50

4

Learning Objectives

By the end of this chapter you should be able to:

- 1Explain why the capital structure decision, the mix of debt, equity, and hybrid securities, is a founder's highest-stakes financial choice, setting ownership, control, and cash obligations at each round.

- 2Describe the debt-to-equity spectrum and why equity is the costliest capital even though no cash leaves the company.

- 3State and apply Modigliani-Miller Proposition I and II in a frictionless world, and show how the 1963 tax correction makes the interest tax shield add value equal to Tc times debt.

- 4Use the tradeoff theory to locate an interior optimal leverage that balances the marginal tax shield against the marginal cost of financial distress.

- 5Explain the pecking order theory and how information asymmetry and adverse selection drive the preference for internal funds, then debt, then equity, and why startups typically must invert that order.

- 6Analyze how agency costs and signaling shape the financing decision, including asset substitution, free-cash-flow discipline, and debt as a credible signal.

- 7Compute the weighted average cost of capital from its components, and reframe a startup's cost of equity as the permanent ownership it surrenders.

- 8Evaluate the debt instruments available to startups and the tax-shield caveat, and explain what the empirical evidence shows about how new firms actually finance themselves.

- 9Assess how the capital stack evolves across the lifecycle, when venture debt extends runway versus becoming a cliff, and the control, signaling, and rich-versus-king dimensions beyond money.

Part One: The Capital Structure Decision Is a Founder's Highest-Stakes Financial Choice. Section 1 of 8.

Part One · The Capital Structure Decision Is a Founder's Highest-Stakes Financial Choice

The Capital Structure Decision Is a Founder's Highest-Stakes Financial Choice

Part One

The Capital Structure Decision Is a Founder's Highest-Stakes Financial Choice

Capital structure is the mix of debt, equity, and hybrid securities a company uses to finance itself. For a founder it is the highest-stakes financial decision, because it sets who owns the company, who controls it, and how much cash the company parts with to survive.

The Highest-Stakes Financial Choice

Capital structure is the mix of debt, equity, and hybrid securities a company uses to finance itself. For a founder it is the highest-stakes financial decision, because it sets who owns the company, who controls it, and how much cash the company parts with to survive. The choice is not made once. It is made again at every round, and the effects compound.

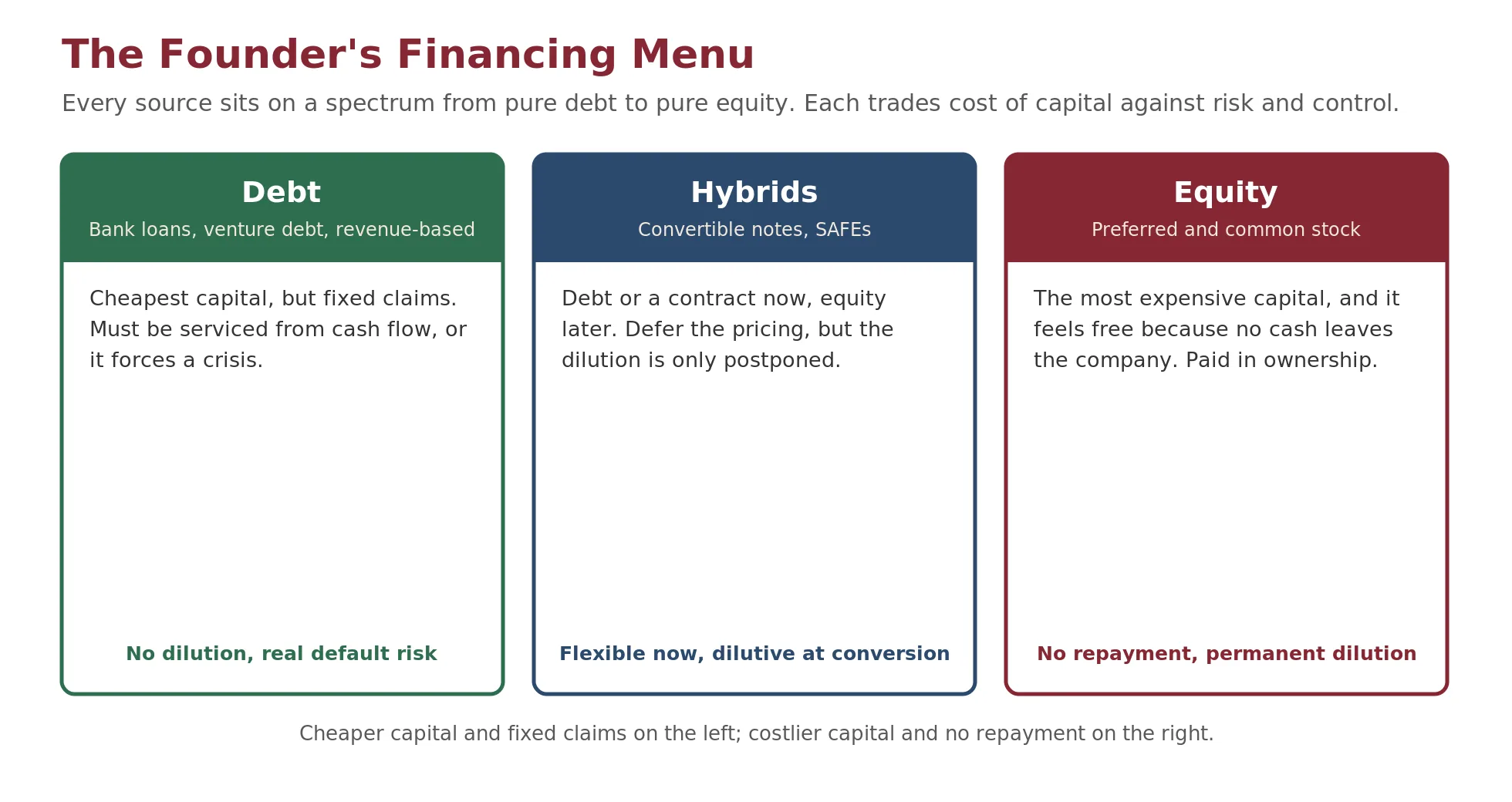

Every financing source sits on a spectrum from pure debt to pure equity.

Debt is a fixed claim. It must be serviced from cash flow on a schedule, whatever the company's fortunes, and it is senior to equity in a liquidation. It is the cheapest capital, because the lender's return is capped and its claim is protected. Equity is a residual claim. It is paid last, carries no repayment obligation, and is the most expensive capital, because it is paid in permanent ownership of all future value. Hybrids, the convertible notes and SAFEs, sit between the two: debt or a contract now, equity later, deferring the pricing but only postponing the dilution.

The Central Question of This Module

The central question of this module is which of these a company should use, in what order, and at what cost. The classical theory answers that question for a mature, profitable firm. Much of the interest, and the irony, lies in how those answers change, and sometimes invert, for a startup.

Check Your Understanding

Knowledge Check 1

Capital Structure & Venture Debt

Why is equity often called the most expensive form of capital, even though no cash leaves the company?