The VC Industry and Fund Economics

The other side of the table: how the venture capital business itself works. Why VC is a small, concentrated asset class with winner-take-most firm dynamics; how it differs from private equity buyout; the three legal entities of every fund (the limited partnership, the management company, and the general partner); the 2-and-20 model of fees and carried interest; the four-tier distribution waterfall and American vs. European timing; the fund lifecycle and the J-curve; performance measurement with DPI, RVPI, TVPI, MOIC, and IRR; why returns follow a power law rather than a bell curve; performance persistence; and how to access the asset class and build a career around it, with four interactive calculators.

125 min

19

49

5

Learning Objectives

By the end of this chapter you should be able to:

- 1Explain why venture capital is a small, concentrated asset class with winner-take-most dynamics at the firm level.

- 2Contrast venture capital and private equity buyout on ownership, leverage, return shape, and value creation.

- 3Describe the three legal entities of a VC fund (the limited partnership, the management company, and the general partner) and what each does.

- 4Analyze the 2-and-20 model, computing management fees and carried interest, and explain why fees dominate manager revenue for the average fund.

- 5Work the four-tier distribution waterfall (return of capital, preferred return, GP catch-up, and the carry split) and distinguish American from European waterfalls.

- 6Explain the fund lifecycle and the J-curve, including capital calls, reserves, and the commitment and harvest periods.

- 7Measure fund performance with DPI, RVPI, TVPI, MOIC, and IRR, and explain what each metric captures and hides.

- 8Explain why venture returns follow a power law rather than a normal distribution, and how that reshapes portfolio construction.

- 9Describe performance persistence, the ways to access venture capital as an asset class, and the careers and advisory ecosystem around it.

Part One: Venture Capital Is a Small, Concentrated Asset Class. Section 1 of 8.

Part One · Venture Capital Is a Small, Concentrated Asset Class

Venture Capital Is a Small, Concentrated Asset Class

Part One

Venture Capital Is a Small, Concentrated Asset Class

Venture capital occupies a peculiar position in institutional finance. It is one of the smallest major asset classes by capital under management, yet it funds an outsized share of the companies that reshape entire industries.

Scale and Concentration

Venture capital occupies a peculiar position in institutional finance. It is one of the smallest major asset classes by capital under management, yet it funds an outsized share of the companies that reshape entire industries. Understanding the industry begins with its scale and its concentration.

By industry estimates from sources such as PitchBook and the National Venture Capital Association, as of 2025 U.S. venture capital firms collectively manage roughly $1.2 trillion in assets. That is a large number until it is set against the roughly $12 trillion U.S. private equity market and the tens of trillions in U.S. public equity. Venture capital is a small pond, and the firms that dominate it are a handful of recognizable names.

Concentration

The concentration is striking. A small number of the largest firms capture a disproportionate share of new capital raised. As of late 2025 and early 2026, based on firm disclosures and press reports, Andreessen Horowitz manages more than $90 billion, and firms such as Sequoia Capital and General Catalyst manage tens of billions each. These are no longer scrappy partnerships writing $1 million seed checks; they are multi-strategy platforms with growth, crypto, and sector-specific funds.

The venture capital industry exhibits the same winner-take-most dynamics it seeks to fund. A small number of firms attract a disproportionate share of capital, deal flow, and returns. The figures here are a 2025 to 2026 snapshot and move over time.

Check Your Understanding

Knowledge Check 1

VC Fund Economics (Fees, Carry, Waterfalls)

How does the U.S. venture capital industry compare in size to public equity and private equity?

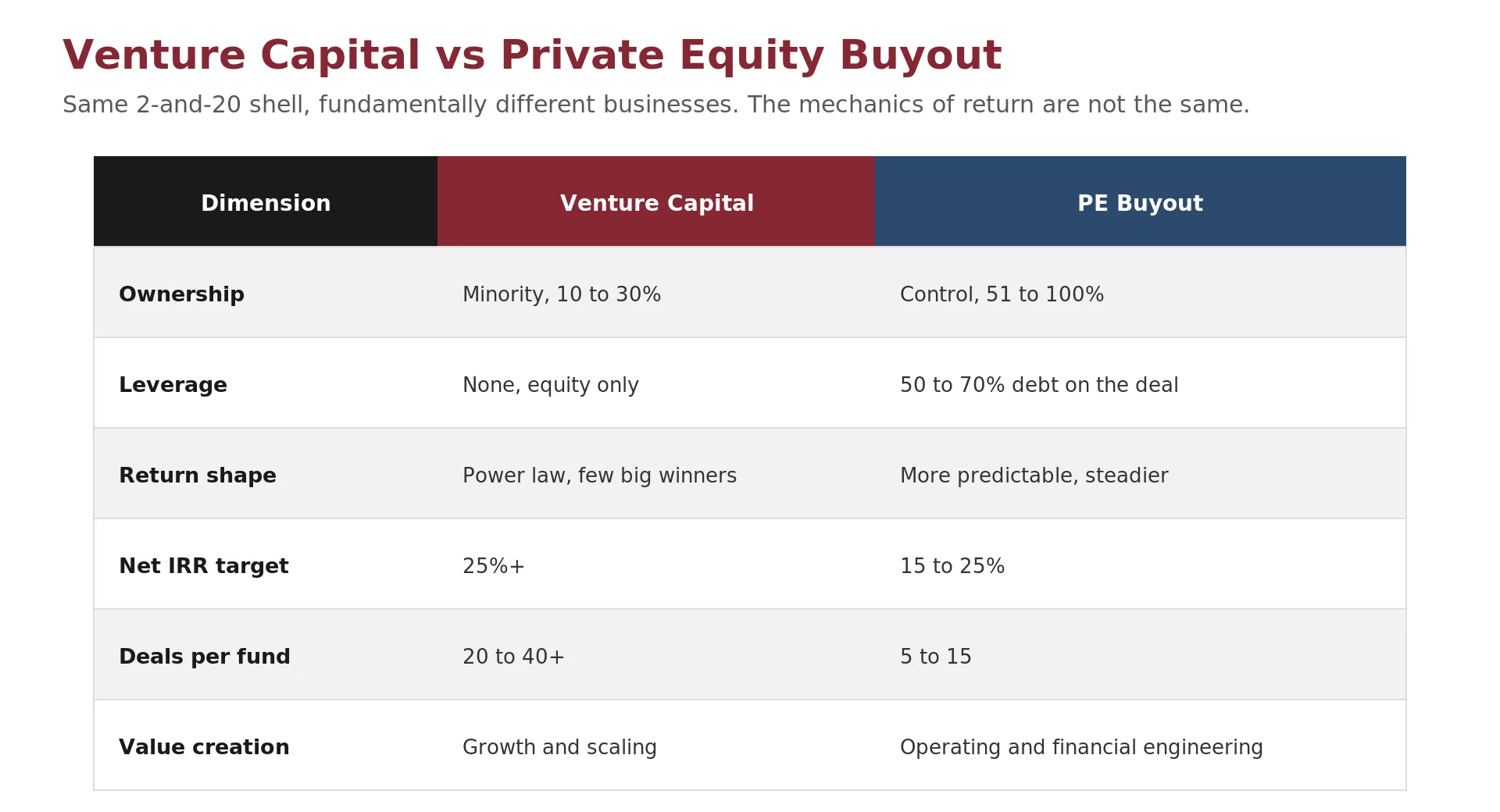

Venture Capital and Private Equity Are Different Businesses

Venture capital and private equity buyout are often grouped together as private capital, and they share the same 2-and-20 fund shell. The businesses themselves are fundamentally different, and the differences are structural, not just a matter of check size.

A venture fund buys a minority stake, commonly 10 to 30%, in a young company and uses no leverage. Its return comes from growth, since a handful of investments must become very large. A buyout fund acquires a controlling stake, 51 to 100%, in a mature, cash-generating company, and finances the purchase with 50 to 70% debt. Its return comes from operating improvements, debt paydown, and multiple expansion, and its outcomes are steadier than the power-law pattern of venture.

These are archetypes. Growth equity sits between them, buying significant minority stakes in scaling companies, and many large firms now run several strategies at once. The mechanics of return remain distinct. Venture depends on rare outliers, while buyout engineers a more predictable result across a smaller number of controlled companies.

Check Your Understanding

Knowledge Check 2

Capital Structure & Venture Debt

What most fundamentally distinguishes a venture capital investment from a private equity buyout?