Financial Forecasting for Startups

How to build a forecast you can defend, a driver-based, bottom-up approach that connects operating assumptions to cash, runway, and enterprise value. Why a forecast is a structured hypothesis, not a prediction; compound growth and CAGR; trailing-twelve-months, run-rate, and NTM as credibility checks; building revenue from the drivers (volume × price) rather than the outcome; eleven guidelines for a clean model; the revenue engine (sales-headcount and subscription MRR models, market sizing); cash as the constraint (gross vs. net burn, runway, minimum cash, and the financing need); unit economics (margins, CAC, LTV, payback, churn, NRR); pipeline, conversion, and headcount timing; stress-testing with sensitivity, scenario, rolling-forecast, and variance analysis; and the MARCS framework that unifies the whole workflow, with five interactive calculators.

130 min

24

50

5

Learning Objectives

By the end of this chapter you should be able to:

- 1Explain why a financial forecast is a structured hypothesis rather than a precise prediction.

- 2Calculate and interpret CAGR, TTM revenue, run-rate revenue, and NTM revenue as tools for evaluating growth and forecast credibility.

- 3Build a driver-based revenue forecast using controllable inputs such as volume, price, sales headcount, productivity ramp, churn, and conversion rates.

- 4Distinguish between outcome-based forecasting and bottom-up forecasting, and explain why bottom-up models are more useful for startup planning.

- 5Construct basic startup cash metrics, including gross burn, net burn, runway, minimum cash balance, and financing need.

- 6Evaluate unit economics using gross margin, contribution margin, CAC, LTV, LTV/CAC, CAC payback, churn, and net revenue retention.

- 7Diagnose forecast risk by using sensitivity analysis, scenario analysis, rolling forecasts, and variance analysis.

- 8Apply the MARCS forecasting framework to clean data, isolate the controllable drivers, build the base case from them, stress-test it against an aspirational stretch overlay, and update the forecast over time.

Part One: A Forecast Is a Structured Hypothesis, and Growth Compounds. Section 1 of 8.

Part One · A Forecast Is a Structured Hypothesis, and Growth Compounds

A Forecast Is a Structured Hypothesis, and Growth Compounds

A Forecast Is a Structured Hypothesis, Not a Prediction

Forecasting is the discipline of using historical data and strategic assumptions to project future states. It converts planning into a rigorous model. In corporate finance, a forecast determines whether a company has the cash to hire, the capacity to expand, or the need to cut costs.

The most important thing to understand is that a forecast is not a prediction of what will happen. It is a structured hypothesis about what could happen, and a framework for responding when reality diverges. The goal is not perfect accuracy; the goal is disciplined preparedness, fast learning, and better decisions as actual results arrive. Accuracy still matters. Forecasts that are consistently wrong without explanation damage credibility with investors, board members, and the team. The discipline is in explaining the variance, learning from it, and improving the next forecast.

This module covers the mechanics: how to build a model from the drivers up, how to stress-test the assumptions, and how to connect the model to the questions founders typically need to answer about cash, runway, and enterprise value. For the line-by-line details of modeling an income statement, Dave Lishego's Founder's Guide to Financial Modeling (2020), a self-published practitioner guide by a venture investment associate, walks through each area with worked examples in Excel. This module focuses on the principles and frameworks that apply regardless of what you are modeling.

Check Your Understanding

Knowledge Check 1

Forecasting & Driver-Based Models

A forecast is best understood as a structured hypothesis rather than a point prediction of what will happen. What is its primary purpose?

Compound Growth Is the Default Trajectory

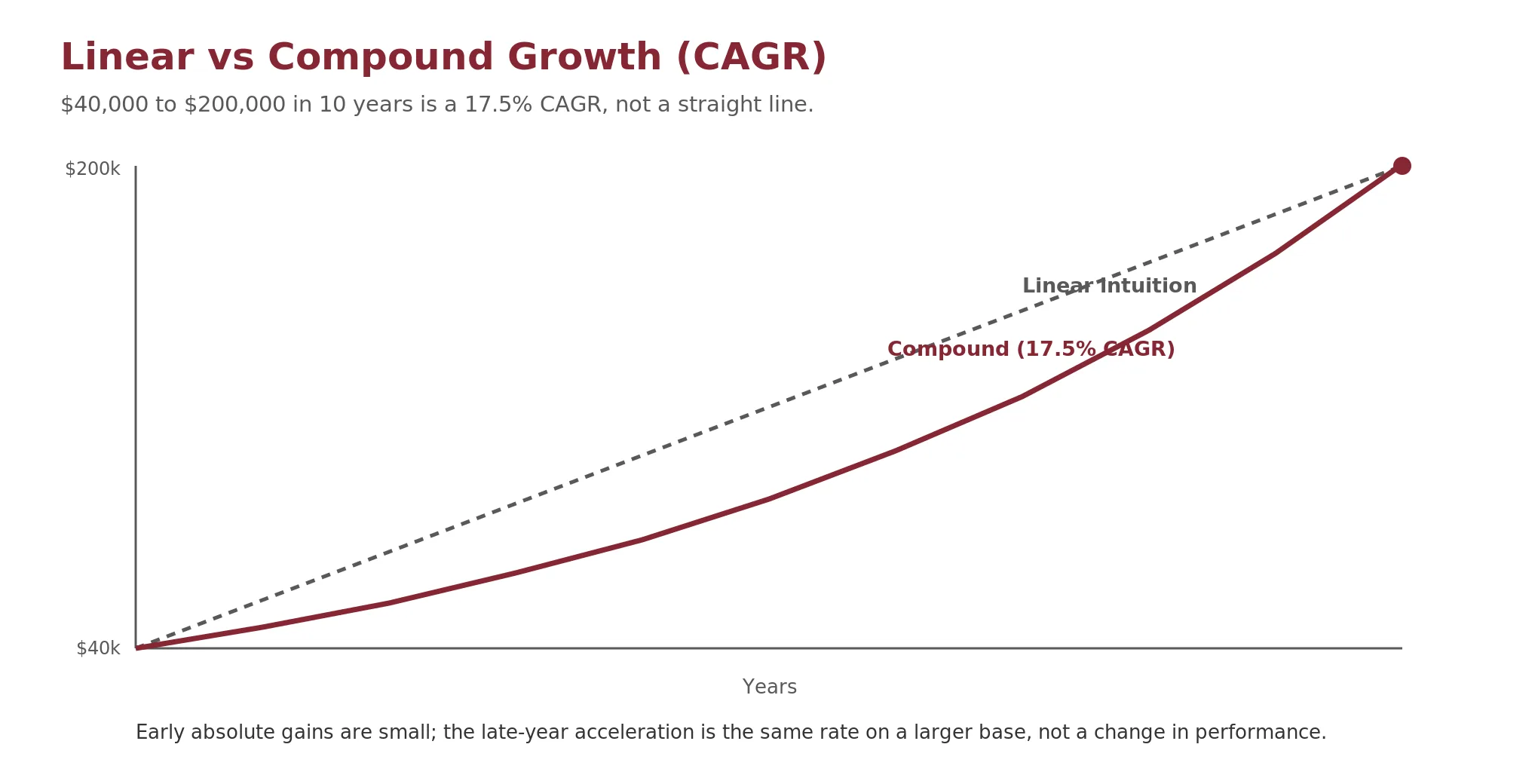

Most people project growth linearly, assuming that if they saved $5,000 this year they will save $5,000 next year. Successful financial trajectories, whether in careers, investments, or business revenue, rarely follow a straight line. They follow a geometric progression. To measure it, analysts use the Compound Annual Growth Rate (CAGR), which smooths the volatility of individual years to reveal the underlying rate required to move from a starting point to an ending point over a period.

Formula. CAGR = (Ending Value / Beginning Value) ^ (1 / n) - 1 where n is the number of years

Worked example: A career trajectory

An entry-level employee earning $40,000 aims to earn $200,000 within 10 years. They are not looking for linear raises. They are solving for a CAGR of about 17.5%: ($200,000 / $40,000) to the 1/10 power is 5 to the 0.1 power, which is about 1.175, minus 1. Consistent annual raises of roughly 17.5% are required to hit the target.

Understanding CAGR changes how you view the early years of any growth curve. On a compound curve, the absolute dollar growth in the early years is small even when the percentage growth is high. The vertical acceleration in later years is not a change in performance; it is the same rate applied to a larger base. This is true for salaries, for startup revenue, and for investment returns.

Adjust the beginning value, target, and horizon to see the CAGR. The defaults reproduce the worked example above.

Interactive Tool

Compound Growth (CAGR)

CAGR

17.5%

constant annual rate

Total growth

5.0×

end ÷ begin

First-year gain

$6,985

same rate, small base

Final-year gain

$29,732

same rate, larger base

The late-year acceleration is not better performance, it is the same 17.5% rate on a larger base. Straight-line intuition would add about $16,000 every year; compounding back-loads the dollars.

Check Your Understanding

Knowledge Check 2

Forecasting & Driver-Based Models

An employee earning $40,000 wants to reach $200,000 in 10 years. What constant annual growth rate would they need to sustain?